FARMlogU

The SaaS infrastructure for LATAM agricultural production. We start with EGGlogU (poultry, live 2026-05). The FarmLogU umbrella expands to other species based on market validation — each new vertical follows the same naming convention, and product derivatives (meat, milk, leather, honey, etc.) are organized by species as the market demands them.

Executive summary

LATAM has 5.2M agricultural producers. 95% keep records in notebooks or Excel. SAP/Oracle Agribusiness costs $50k–$200k USD/year, runs in English and requires 6–12 months of consulting. Zero options between $0 and $50k.

FarmLogU fills that gap with vertical-specific modular SaaS ERP: $0–$199 USD/month, neutral Spanish, mobile-first, offline-resilient, AI built-in from day one.

$500k USD seed (pre-money $4-6M, target dilution 10-15%) to reach 500 paying customers (~$50k MRR) and validate the priority of the second vertical under the FarmLogU umbrella (the species/product is chosen with real data post-EGGlogU launch).

| Use of funds | % | USD approx | Milestones covered |

|---|---|---|---|

| Engineering + product | 60% | ~$300k | 2 hires (vet + senior eng) · stack scaling · LogU AI inference |

| Go-to-market | 25% | ~$125k | Vet rep commissions · vet content · onboarding · events |

| Legal + compliance | 10% | ~$50k | Term sheet · B2G contracts · INAPI additional classes · privacy |

| On-premise AI hardware | 5% | ~$25k | Training + inference workstation (24m TCO lower than cloud GPU) |

Before signing an NDA, opening a data room or discussing a term sheet, I propose a 30-minute conversation. No commitment. No fee. Zero paperwork up front.

On that call you ask every question you need: real traction, team, technology, competition, financial model, exit, anything. I respond with verifiable data and acknowledge what is still projection. If there is mutual fit after that, we move to NDA + data room. If not, it stays as a good conversation between two people who respect each other's time.

To schedule: jadelsolara@egglogu.com with your availability and time zone. I confirm within 24 hours.

Problem

LATAM has several million active agricultural producers (FAO estimates and national censuses converge on 5–6 million orders of magnitude). The vast majority share five structural problems:

- Notebook or Excel records → data gets lost, zero forecasting

- No traceability → export blocked by new GS1, SAG Chile, USDA APHIS and equivalent LATAM regulator requirements

- Buying inputs at wholesale price due to lack of alternatives → significant overspend

- Late outbreak detection → high preventable mortality from Newcastle, IBD, avian influenza and similar diseases

- Accounting 6 months late → zero visibility into per-batch / per-cycle costs

Enterprise ERPs (SAP Agribusiness, Oracle, Microsoft Dynamics 365) do exist but typically cost tens to hundreds of thousands USD/year, require 6–12 months of implementation consulting, and are mostly offered in English and Brazilian Portuguese. Inaccessible to the vast majority of the LATAM market.

It's not a technical problem — it's a market that requires vertical depth + LATAM cultural fit + accessible pricing simultaneously. It's the "Stripe gap" (pre-Stripe LATAM couldn't charge online) applied to agriculture. Building it right requires a technical, bilingual founder committed to accessible margins.

Solution

FarmLogU = modular SaaS ERP per agricultural vertical. Each vertical has its own brand but shares the same stack:

Only EGGlogU is live today. Next vertical is chosen with real post-launch data, not a fixed roadmap.

| Vertical | Brand | Status | Launch |

|---|---|---|---|

| Poultry (hens · eggs) | EGGlogU | Live | 2026-05 |

| Future verticals: under the FarmLogU umbrella, other species are added as the market demands them — cattle, swine, beekeeping, aquaculture. Each new brand follows a simple, consistent naming convention, and product derivatives per species (meat, milk, leather, honey, wax) are organized later with real market data. EGGlogU is the first instance and defines the functional and technical model that gets replicated in each new vertical; demand picks the order, not a predefined plan. | |||

Shared stack (high level)

- Proprietary AI layer — vertical models focused on early outbreak alerts, productive forecasting and species-specific recommendations. Status: functional prototypes under internal evaluation, validation tests in progress before the first real cohort. Architecture and naming under NDA.

- Multi-tenant backend with per-organization database-level isolation (production-grade)

- PWA + offline-resilient mobile app — works without connectivity, syncs on reconnect (live)

- LATAM recurring payments — multi-country charging in native local currency (live)

- 16 languages — neutral Spanish as an educational vector for LATAM rural areas (live)

5 structural differentiators

- Vertical depth — each vertical understands its own parameters (FCR for poultry, ADG for cattle, biomass for aquaculture)

- AI built-in from day one (not an add-on) — predictive alerts, recommendations, forecasting. Validation tests in progress, final adjustments before the first real cohort.

- GS1 traceability from day one — EU/USDA export-ready without extra work (architecture already supports it; regulatory certification on roadmap)

- Accessible pricing — $0 to $199 USD/month range (4 public tiers, live)

- On-demand AI assistant — in validation, production roadmap Q3-Q4 2026 (details under NDA)

Proprietary technology. Model naming, internal architecture, datasets and granular technical stack available under mutual NDA + time commitment + confirmed minimum investment ticket.

Why now

The LATAM agri market has had this same problem for decades. What changed in the last 18 months makes 2026 the optimal window to build FarmLogU:

1 · Traceability regulation forces digitalization (or you're locked out)

The EU is tightening GS1 traceability requirements for animal protein imports starting in 2026. SAG Chile, SENASA Argentina, USDA APHIS and MAPA Brazil are moving in the same direction. Producers who don't digitalize lose access to premium export markets. Notebook and Excel stop being an option — not by preference, by compliance.

2 · Record HPAI outbreaks 2023-2025 make health the #1 priority

Highly pathogenic avian influenza caused mass culls in the US, Europe and parts of LATAM in 2023-2025. The cost is unforgettable: every poultry producer today knows that an undetected outbreak equals losing the whole batch. Demand for early alerts + predictive AI no longer requires convincing.

3 · Generative 70B+ AI became commoditized in 2024-2025

Open-source 70B-parameter models (Llama 3.3, Qwen 2.5, DeepSeek V3) now run on a $10k workstation. 24 months ago this required a $500k cluster. Proprietary vertical AI is economically viable for the first time, without depending on OpenAI/Anthropic APIs or expensive cloud rental.

4 · MercadoPago LATAM-wide recurring preapproval matured

MP now supports SaaS recurring card billing in CL/AR/MX/BR/CO/PE/UY/EC natively via the preapproval API. Pre-2023 this required a payment provider per country and per-jurisdiction compliance. Today a single integration covers 95% of the LATAM market in the customer's local currency.

5 · Rural LATAM smartphone penetration crossed 80%

The median LATAM producer in 2026 has a decent Android phone + 4G data on the farm (varies by region). 10 years ago "mobile app for the farmer" was science fiction. Today it's the natural channel. PWA + offline-resilient covers even areas with intermittent internet.

6 · High cost-of-capital makes enterprise ERPs unviable (opportunity)

High LATAM interest rates 2024-2026 + producer margin pressure = SAP/Oracle at $50-200k/year are even less viable than in 2020. The "pricing $0-$200/mo" gap is bigger than ever. What looked niche 5 years ago is today a structural market need.

7 · Argentina economic distress + regional export pressure

Post-distress Argentina 2024-2025 created producers who need affordable tools in pesos to survive; Chile is pushing premium export to compensate for the domestic market; Mexico is digitalizing for USDA APHIS compliance. Three large markets with different motivations but the same need.

Regulation + outbreak history + commoditized AI + mature multi-country payments + rural smartphones + unviable expensive ERPs + export pressure = an 18-36 month window for FarmLogU to define the category. After that, others will attempt the same space. The opportunity is now.

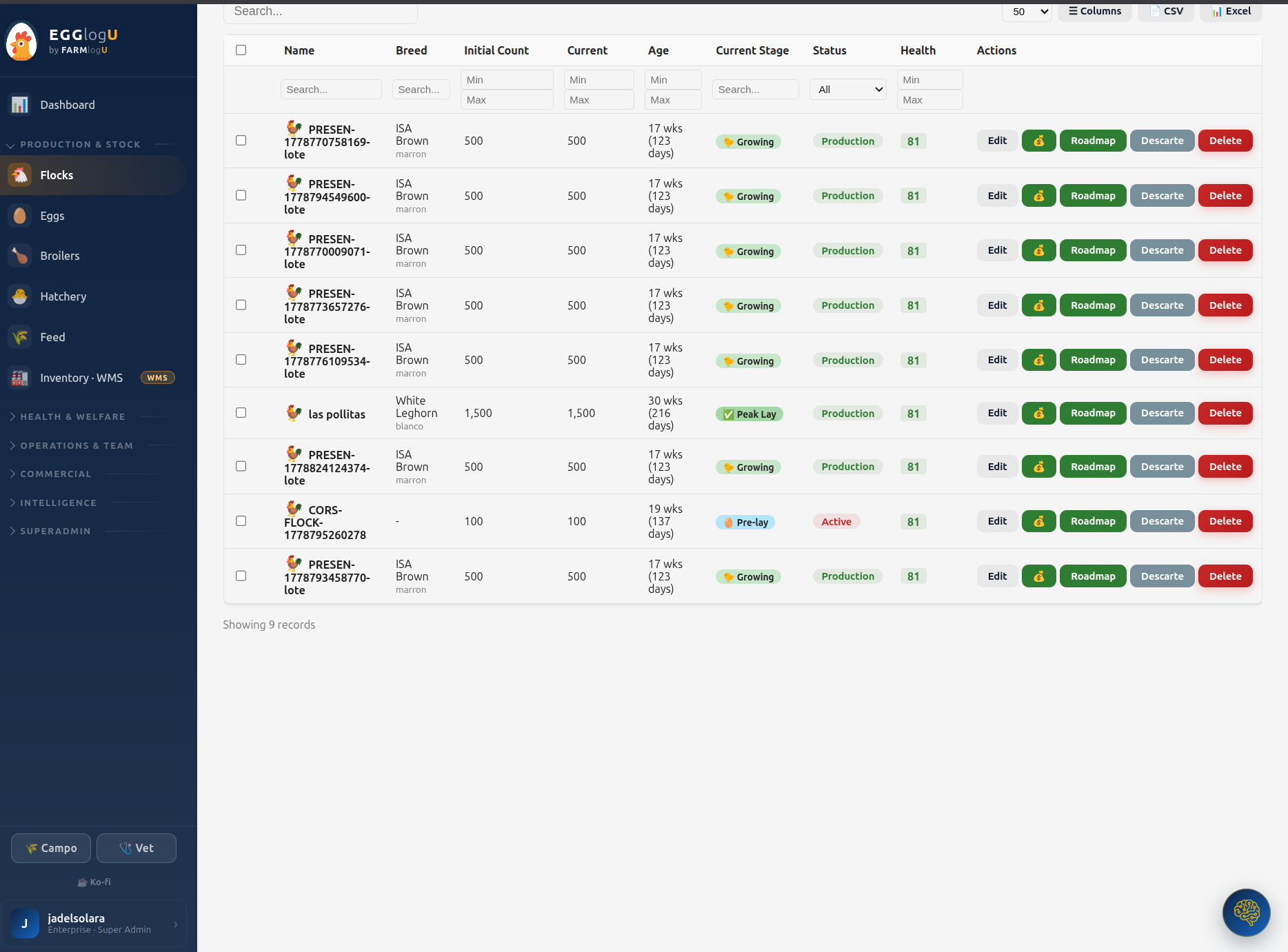

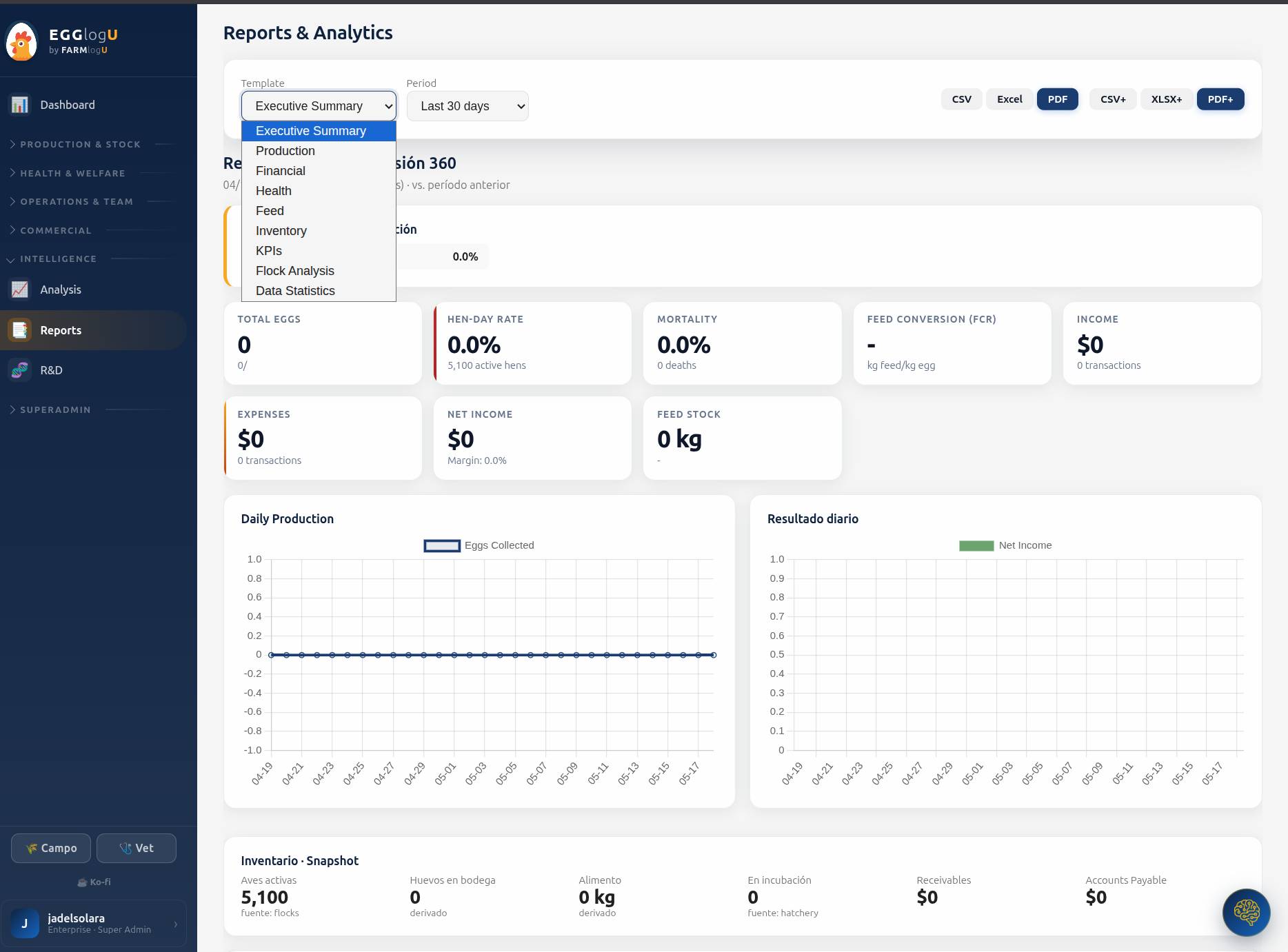

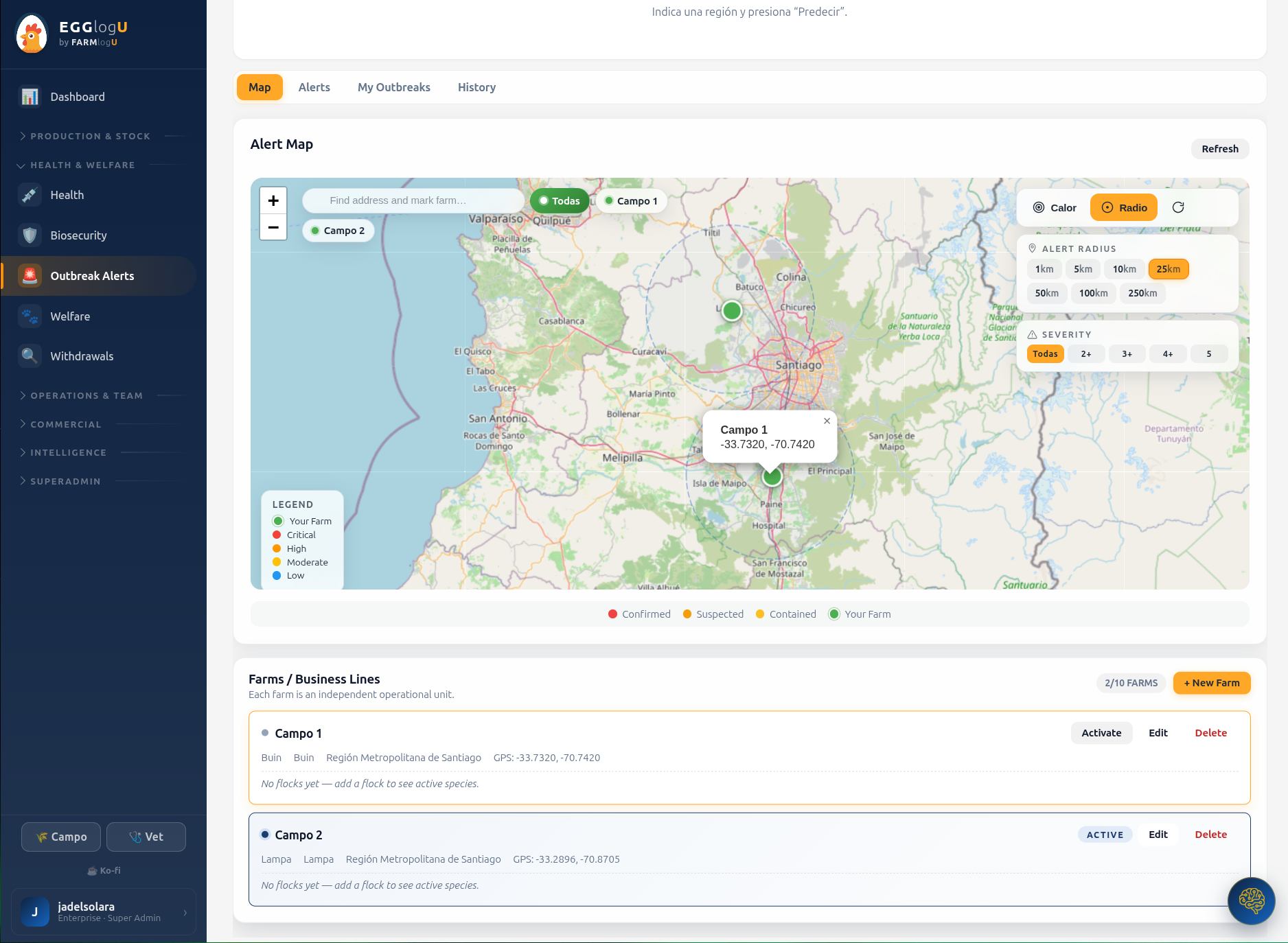

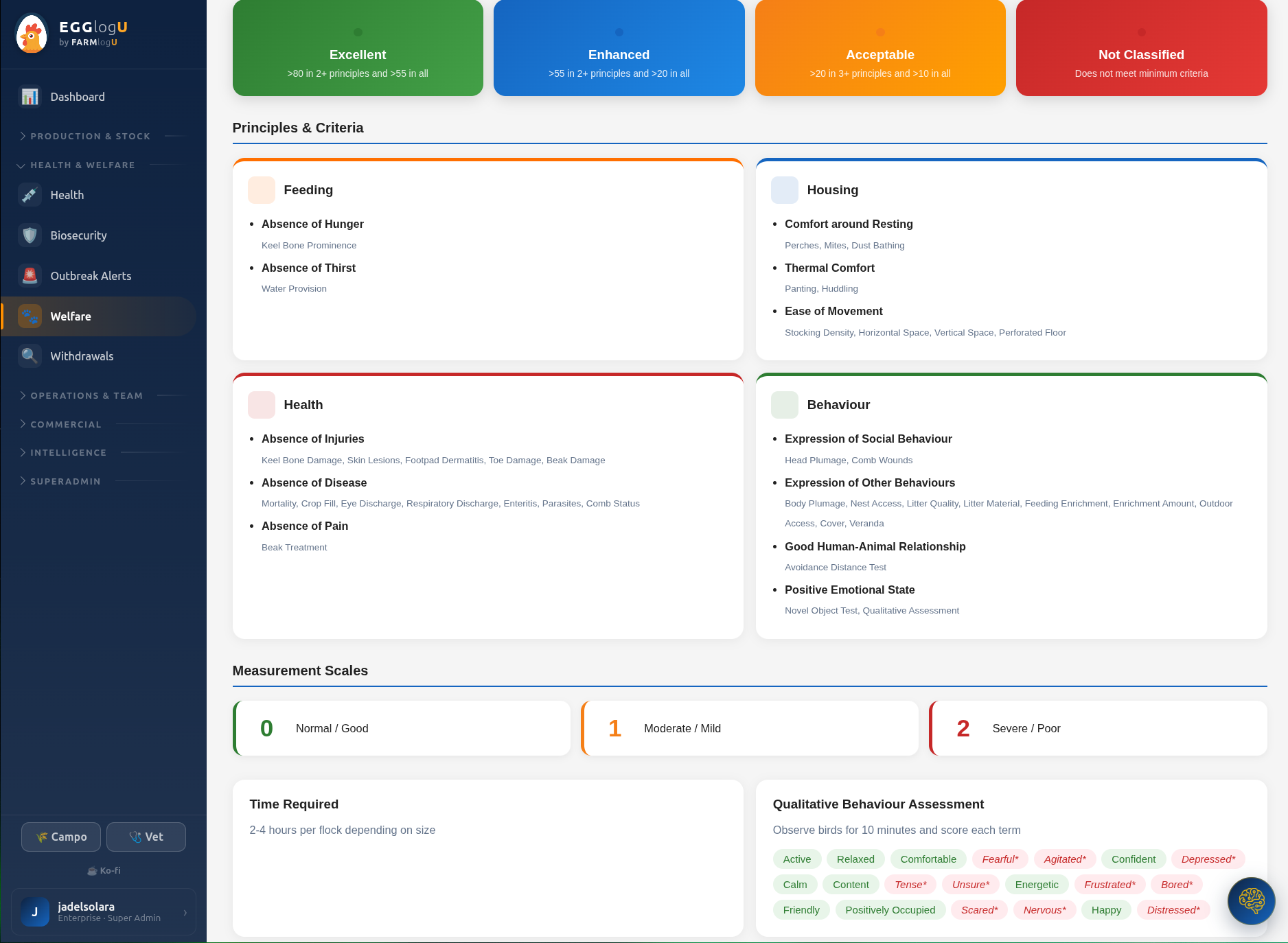

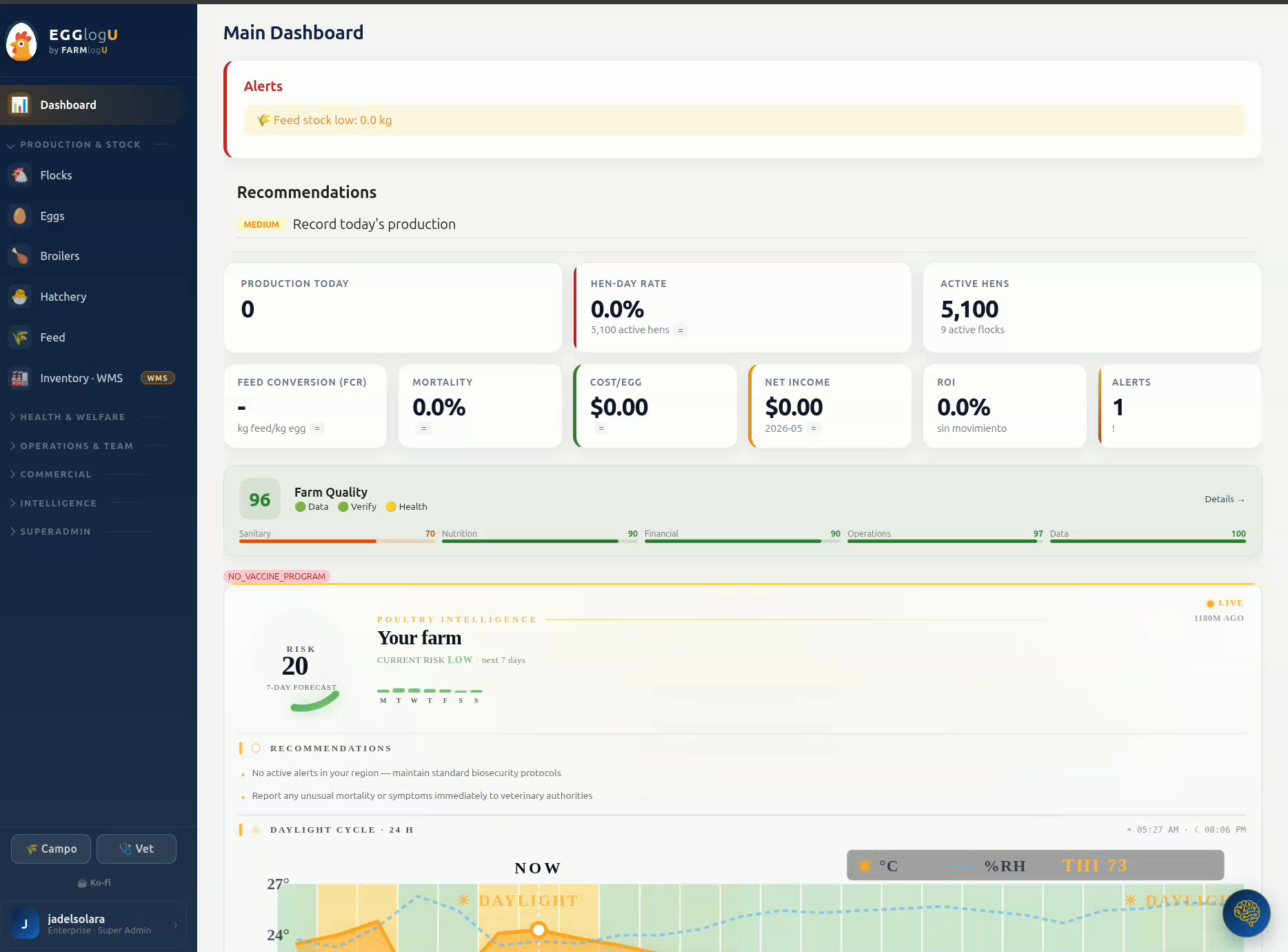

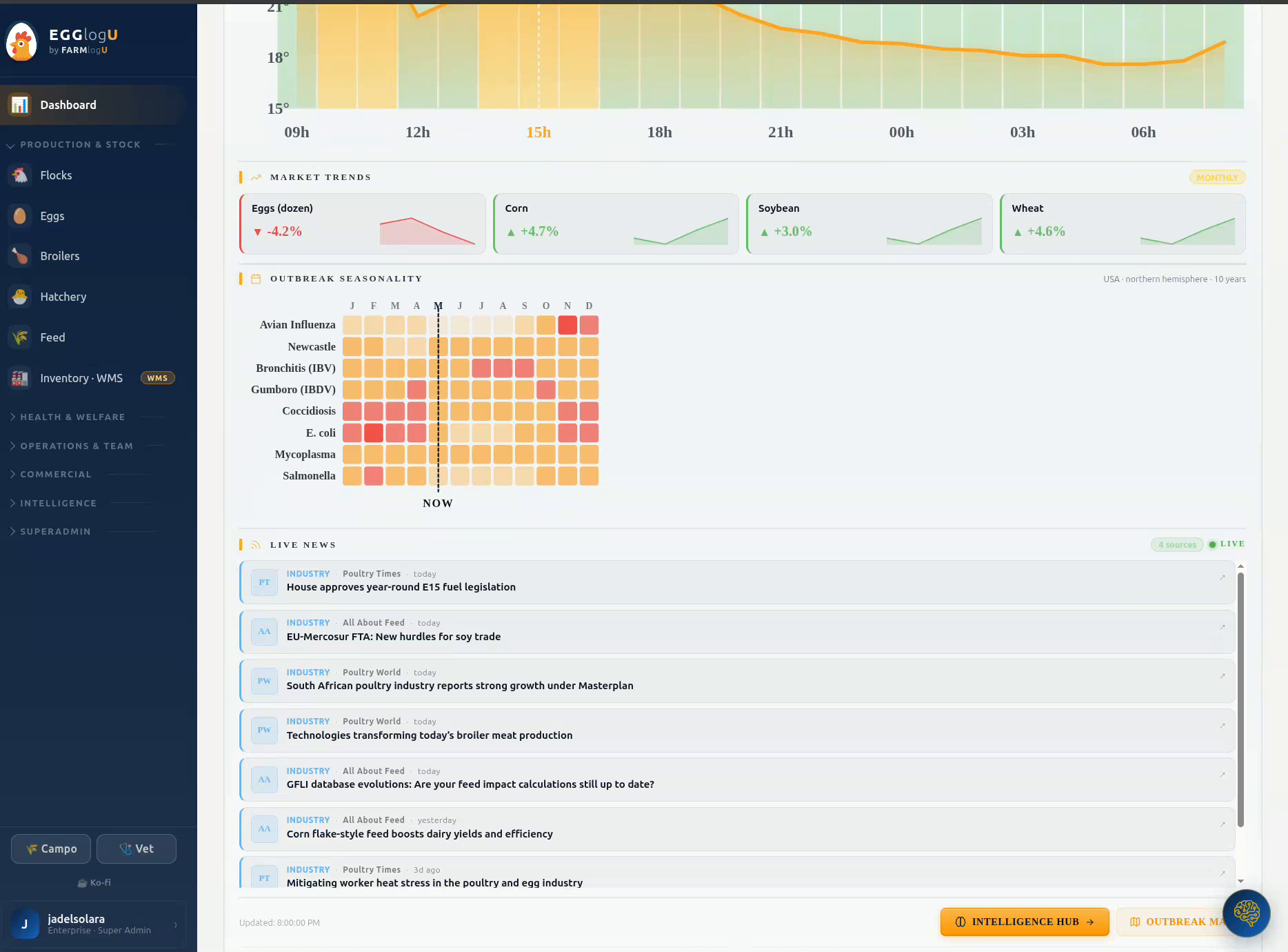

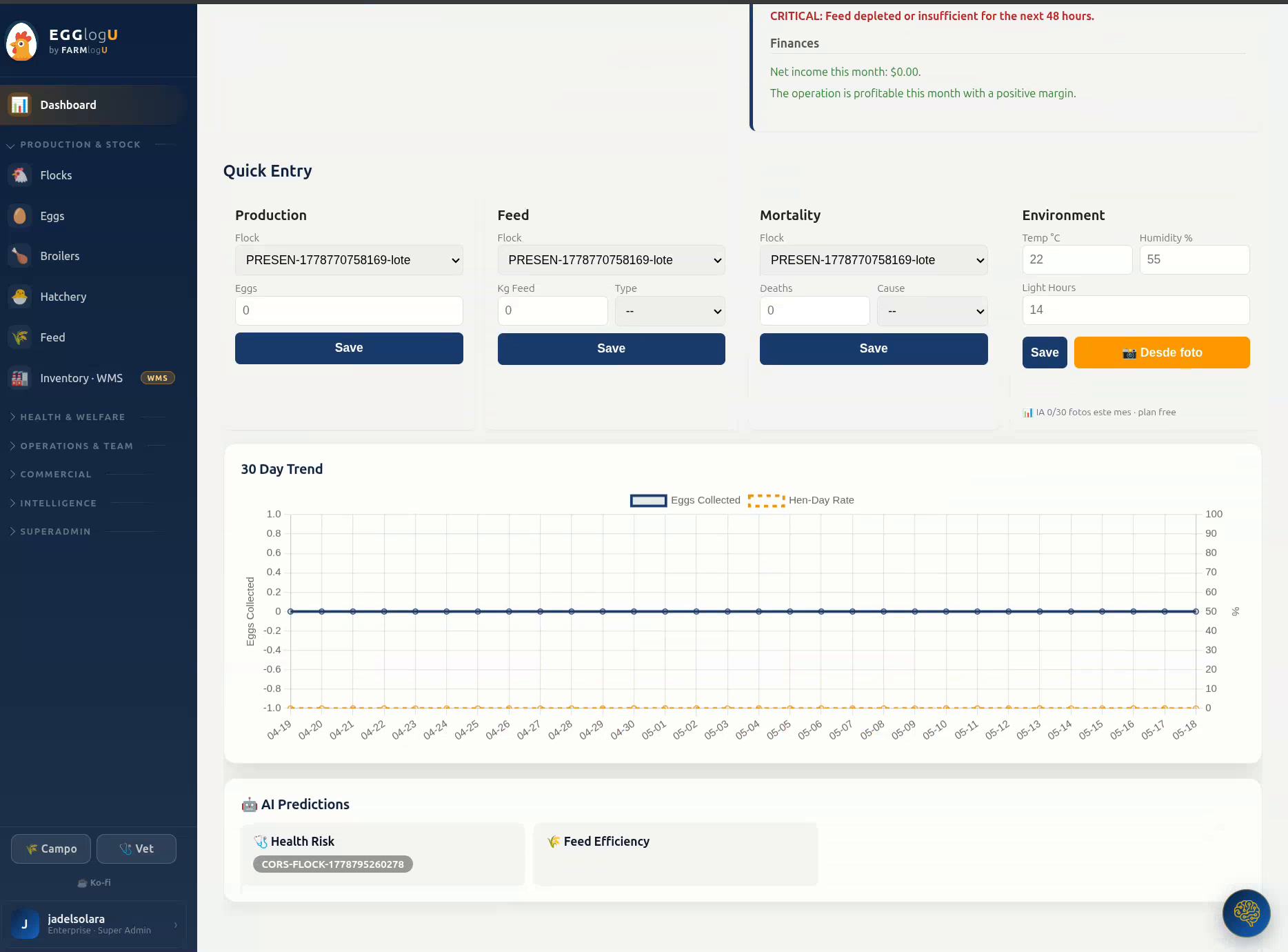

Product — EGGlogU as the first instance

Dashboard walkthrough — additional views (click any to enlarge):

Active features today

- Multi-farm, multi-batch, multi-user

- Daily production, collection, egg quality

- Health: vaccines, treatments, mortality, outbreak alerts

- Broiler fattening + hatchery

- Customers, sales, inventory, dispatch

- Finance, purchasing, payroll, reports

- GS1 traceability + Excel/PDF export

- Offline mobile app (48h) + 16 languages

Technical maturity

- Product running 24/7 in production with complete E2E test suite

- Bank-grade backup infrastructure (4-nines)

- Sustained development velocity (daily commits)

- 16-language coverage to scale LATAM + global when appropriate

- Multi-tenant with per-organization data isolation

Tech stack

Modern production-grade stack: cloud-native backend with Postgres, edge-deployed frontend, mobile-first offline-resilient PWA, next-generation passwordless auth, native LATAM recurring payments. Detailed architecture diagram available under NDA.

Vertical hardware integration — roadmap

Software solves the management layer. The next value layer is on-farm hardware integration: sensors that feed the system with real-time data so recommendations and alerts become more precise, actionable and differentiated.

Planned sensor integrations (via open protocols like MQTT and HTTPS, manufacturer-agnostic):

- Ammonia (NH₃) — early detection of poor ventilation

- CO₂ — air quality and energy efficiency

- Temperature & humidity — thermal comfort per shed

- Lighting — automated lighting programs

- Water consumption — early mortality / disease alert

- Feed consumption — real-time FCR

- Automatic weighing — growth curve without handling

- Cameras + computer vision — behavior, counting, health

Why it matters: each sensor turns a blind spot into a continuous signal that enriches the vertical AI model. More data density = better early alerts, more precise recommendations, producer decisions with less guess-work. It's the difference between "logging what happened" and "anticipating what's about to happen."

Commercial model: staged evolution — Y1 integration with already-installed sensors via open APIs, Y2 partnerships with selected manufacturers and white-label basic kits, Y3+ curated catalog of compatible best-in-class accessible hardware. Producer picks what to activate based on budget and priority. Full plan + partnership roadmap available under NDA.

Market

Note: the following TAM/SAM/SOM ranges are internal FarmLogU estimates based on public LATAM agricultural censuses and regional B2B SaaS benchmarks. Figures to be refined during seed-round market due diligence. The $1,000/year ARPU assumption reflects progressive penetration of paid tiers + addons (not the initial Free/Starter ARPU). Real bottom-up adoption per tier and per-country sensitivity are in the data room post-NDA.

LATAM poultry (Year 1 focus) — internal estimates

FarmLogU multi-vertical (Years 2-5) — internal estimates

Geographic strategy — Chile HQ + demand-driven expansion

FarmLogU policy: single HQ in Chile (FarmLogU SpA). Multi-country product from day one via global edge infrastructure and a LATAM multi-country payment processor (8-country coverage). 100% online reach. Physical expansion to other countries only when the market signal calls for it (operational thresholds under NDA). If Chile alone sustains us → we stay Chile-only. The product remains accessible to any LATAM market via web.

| Country | Product access (day 1) | Physical setup |

|---|---|---|

| Chile (HQ) | ✓ live | FarmLogU SpA · remote team in Chile |

| Argentina, Mexico, Brazil, Colombia, Peru, Uruguay, Ecuador | ✓ online · MP supports local currency | Only when demand signal justifies it (≥150 accounts + $15k local MRR) |

Competitive landscape

Today no direct competitor in LATAM matches the footprint FarmLogU brings (multi-country · neutral Spanish · built-in AI · offline-resilient · $0-$199/month pricing). Competition is structural — different categories each partially solving the problem, none covering it fully.

The 4 structural categories of competition

| Category | Representative examples | Typical pricing | When we encounter it |

|---|---|---|---|

| Enterprise ERP | SAP Agribusiness, Oracle Agribusiness, Microsoft Dynamics 365 | $50k-200k USD/year + 6-12 months consulting | Large producer tries SAP, finds it costs 20-50× their budget and gives up |

| Hardware-coupled software | Big Dutchman BigFarmNet, equipment-manufacturer monitoring systems | Tied to buying vendor hardware (€10k+ equipment) | Producer with modern industrial hardware, locked into the manufacturer's closed ecosystem |

| Local sub-country vertical SaaS | Regional software in Chile/Argentina/Mexico/Brazil — multiple small providers per country | $20-150 USD/month (high variance) | Producer adopted local software years ago; works for their country but doesn't scale multi-country, no AI, no robust offline, generally outdated UI |

| Spreadsheets + WhatsApp + notebook | Excel, Google Sheets, notebooks, WhatsApp groups | $0 | ~95% of the LATAM market today. The largest "competitor" by volume. |

Defensible mapping — 3 layers of competition

Recommended DD framing: the agri software market splits into three vertical layers. Each real company occupies a specific layer. EGGlogU (poultry-specialized) competes primarily with Layer 2; Layers 1 and 3 are indirect adjacencies with partial fit.

Layer 1 — Enterprise agri ERP (high indirect)

| Company | Origin | Fit vs EGGlogU |

|---|---|---|

| SAP Agribusiness | Germany · global | High indirect · top-tier corporates · pricing in tens-hundreds k USD/year |

| Microsoft Dynamics 365 | USA · global | High indirect · generalist ERP · requires local implementation partner |

Layer 2 — Poultry management specialized (direct) ← where EGGlogU competes

| Company | Origin | Fit vs EGGlogU |

|---|---|---|

| MTech Systems (mtechsystems.io) | USA | High direct · cloud poultry flock management, performance, costing, planning |

| Big Dutchman BigFarmNet | Germany | Partial direct · strong poultry, tied to environmental control and own hardware |

| Cumberland / Hog Slat / GSI | USA | Partial direct · hardware-coupled, strong USA poultry |

| Porphyrio (Huvepharma group) | Belgium | Partial direct · analytics/genetics/production for breeders and integrators · not a broad ERP |

| Aviapp (Huvepharma) | Belgian cloud poultry app | Low-medium direct · cloud poultry data app |

| PoultryPlan | USA / global poultry software | Partial direct · poultry farm management software; verify specs and current LATAM footprint on their official site before citing in DD |

Layer 3 — Generalist agri management (medium indirect)

| Company | Origin | Fit vs EGGlogU |

|---|---|---|

| AGRIVI (agrivi.com) | Croatia · Europe | Medium indirect · generalist farm management (multi-crop) with AI + traceability + IoT/ERP. NOT poultry-specialized — adjacency, not direct rival |

| Hispatec (hispatec.com) | Spain · LATAM presence | Medium indirect · broad agri-food suites, multi-crop |

"AGRIVI is a generalist farm management competitor and an indirect adjacency to EGGlogU, not a pure poultry ERP competitor." — Same logic applies to Hispatec. EGGlogU competes primarily in Layer 2 (poultry-specialized) against MTech / BigFarmNet / Cumberland / Porphyrio / Aviapp. SAP and Dynamics (Layer 1) are indirect enterprise; AGRIVI and Hispatec (Layer 3) are adjacencies in agri digital budget, not pure poultry use case.

No player across these 3 layers simultaneously combines: native LATAM multi-country focus · price accessibility · integrated vertical AI · offline capabilities + multi-vertical roadmap · government regulator alliance. The intersection of these attributes defines the space FarmLogU occupies.

5 reasons we win each category

- Vs Enterprise ERP: 100× more accessible in pricing. SAP requires an $80-200/hour consultant for 6-12 months. FarmLogU activates in 2 hours with a veterinary advisor on site.

- Vs Hardware-coupled: manufacturer-agnostic. We work whether the producer has Big Dutchman, Cumberland or hand-built sheds. Public APIs for open integration.

- Vs local sub-country SaaS: multi-country from day one (global edge infrastructure + LATAM-wide payment processor) + built-in vertical AI (not an add-on) + educational neutral Spanish + 48h offline + multi-vertical roadmap (poultry → aquaculture → cattle → agri → beekeeping).

- Vs Spreadsheets/WhatsApp: a producer who adopts FarmLogU gets GS1 traceability (export compliance), predictive outbreak alerts (proprietary AI layer in validation), and automatic per-batch/per-cycle cost recording — things Excel + WhatsApp never give them.

- Unique regulatory moat: epidemiological API for the state regulator (SAG/SENASA/SENASICA/MAPA) that no structural competitor has. When the regulator depends on our signal for national surveillance, switching cost becomes insurmountable.

FarmLogU provides the state regulator with an epidemiological surveillance API delivering anonymous, geo-referenced aggregated mortality and symptom data in real time. The government detects potential outbreak spikes in hours rather than weeks — targeted dispatch over affected zones instead of random inspections.

- Privacy by design: no individual producer information (guaranteed k-anonymity · regional aggregates only · GDPR / national data protection compliance).

- Open replicable spec: aligned with Open Market doctrine — any competitor can offer the same API; the structural advantage comes from signal density (volume of active accounts reporting clean data).

- B2G revenue model: API access is charged to the state regulator via institutional subscription. Live outbreak data carries substantial regulatory value — it is NOT a free hand-out; it is a revenue stream parallel to B2B SaaS.

- Regulator switching cost: when the regulator depends on this signal for national surveillance, migrating to another provider = rebuilding the country's epidemiological infrastructure. That's years, not months.

Outcome for the government — food sovereignty: this is NOT just analytical data for the regulator; it is direct prevention of impacts on the country's food supply. An undetected outbreak = mass mortality in farms = scarcity of accessible animal protein for the population + inflationary pressure on the basic food basket. The API turns reactive late-stage inspection into early preventive intervention.

Full technical spec + endpoints + privacy model + B2G pricing + integration with regulator's existing systems available under mutual NDA.

Local LATAM vertical SaaS providers exist but are small shops (1-5 people, no AI, no modern mobile app, legacy UI). Our plan is NOT to compete with each one separately — it's to create the category "LATAM-wide, AI-native, accessible agricultural SaaS" that doesn't exist today. When a producer compares FarmLogU against their country's local software, the decision is typically obvious. The real fight is against the inertia of Excel + notebook, not a specific SaaS competitor.

Traction (as of 2026-05-18) — first pilot collaboration committed (pre-launch)

- 1 pilot collaboration committed · pre-launch — a first laying-hen farm is preparing to deploy the system. Initial flock of approximately 2,000 laying hens is expected to arrive at the farm by the end of May 2026 (target flock size: ~5,000 birds). The pilot starts operation once the flock is on-site. Zero continuous pilot data yet (the birds are not at the farm yet).

- Zero paying users to date (pilot in operational validation phase · monetization planned post-cohort expansion).

- Real MRR: $0 until first paying cohort closes (Month 1-3 post-seed).

- Zero confirmed waitlist in commercial format.

- Technical product launched May 2026 — already running in real production on one farm; cohort expansion (~25 customers Q1) starts with the seed investment (vet-led sales force + go-to-market).

Every metric below labeled "target" or "projection" is internal, NOT historical. Investors looking for "early traction of N paying users" should wait until Month 3-6 post-seed close. The committed pilot collaboration is referenceable under mutual NDA once it is running (post-arrival of the flock by end of May 2026).

What IS built and verifiable today

- Operational technical product: production-grade backend, web app + PWA + admin panel + billing flow via MercadoPago LATAM

- Auditable stack: commits + endpoints + e2e specs accessible for technical due diligence

- 16 active languages: Spanish, English, Portuguese, French, German, Italian, Japanese, Chinese, Korean, Russian, Indonesian, Thai, Vietnamese, Swahili, Hausa, Amharic

- Multi-country payments live: recurring billing in CLP, MXN, ARS, COP, PEN with verifiable landing/checkout parity

- Solo founder to date (time + own capital invested, details under NDA)

Internal target metrics Q3 2026 (90 days post-launch)

⚠ Internal estimates. NOT real data. Refined in DD under NDA with documented assumptions.

Internal target metrics Q1 2027 (200 days post-launch)

⚠ Internal estimates. NOT real data. Model + sensitivity analysis under NDA.

Business model

Pricing (USD nominal · CLP landing source of truth)

| Plan | USD | CLP BETA promo | CLP full |

|---|---|---|---|

| Free | $0 | $0 | $0 |

| Starter | $49 | $39,990 | $59,990 |

| Pro | $99 | $79,990 | $119,990 |

| Enterprise | $199 | $159,990 | $229,990 |

Modular add-ons

Catalog of vertical packs that activate on top of each base tier. Pack details, per-pack pricing, minimum required plan and upsell matrix available under NDA + minimum ticket commitment.

Extra users: per-additional-user fee available across all paid tiers.

Gross margin — high level

B2B SaaS model with target gross margin in the industry-standard 85-95% range. Post-Series A target net margin 25-35%. Detailed unit economics (cloud cost per account, processor fees, CAC payback, LTV/CAC) available in the data room post-NDA.

Go-to-market

Vet-Led Sales Force

100% domain-credentialed veterinary sales force (Veeva/Procore/Toast pattern in their respective industries). Detailed operational model available under NDA.

Companion — outcome-based revenue stream

Post-launch complementary product that sells outcomes (productive results to the customer), not licenses. Structural differentiator vs traditional vertical SaaS that sells software. Vet-rep revenue-share model detailed under NDA.

Regulatory alliance (Y2-Y3 moat)

Phased relationship plan with LATAM regulators (SAG, SENASA, SENASICA, MAPA and equivalents). Compatible with our open market policy: traceability protocols are published as an open specification so competitors can adopt them if they wish. Phases and timeline detailed under NDA.

🛰️ B2G epidemiological API — national insurance against food supply crises

FarmLogU offers the state regulator an institutional B2G API delivering anonymous geo-referenced aggregates of real-time mortality and symptomatology. The government detects potential outbreak spikes in hours instead of weeks, with targeted dispatch over affected zones instead of random inspections.

Commercial framing — this is national insurance for the country: the regulator pays a monthly/annual premium for the API and in return receives real-time preventive surveillance against food supply crises (an undetected outbreak = mass mortality in farms = scarcity of animal protein + inflationary pressure on the basic basket). Cost of insurance vs. cost of an inflationary food-supply incident = an asymmetric ratio that is obvious to the ministry of finance.

Privacy: no individual producer information (k-anonymity); Open market: spec is open and replicable by competitors — our advantage comes from signal density (volume of active accounts). Billing model: institutional subscription billed to the regulator (NOT a free hand-out).

Why it's a moat: when the regulator depends on our signal for national surveillance, switching cost = rebuilding the country's epidemiological infrastructure. Full technical spec + endpoints + privacy model + B2G pricing available under mutual NDA.

Crisis Response Network

Rapid outbreak response network with vet-rep dispatch. Public hotline (free in severe distress cases, commercial otherwise). Operational model + economics under NDA.

Team & hiring plan

Founder

José Antonio Del Solar Alemparte — Founder, CEO/CTO, full-stack

Owner: FarmLogU SpA (Chile) · Current cap table: 100% · LinkedIn

Founder compensation — base + monthly commission

The product and business model are already built and ready to scale. What the seed round enables is accelerating impact in the short term — turning bootstrap into a capital-backed operation with a board shared with investors that distributes the load of strategic decisions. The founder's compensation reflects that transition: a sustainable base floor to keep focus on the business vision + a variable MRR commission that naturally aligns the founder with the growth investors expect. Milestone-based bonus structure to be defined in the term sheet alongside the lead investor.

| Stage | Base USD/month | Variable commission | OTE USD/month (reference) |

|---|---|---|---|

| Month 1-12 post-seed (Y1) | $7,000 | — (no commission Y1, focus on cohort build) | $7,000 fixed |

| Month 13+ (Y2 onward) | $5,000 | 5% on sales (net MRR from prior month) | $5k base + 5% MRR · scales with growth |

Philosophy: fixed sustainable base in the first year while the cohort is built without immediate commercial distraction, and starting Month 13 the founder switches to a lower base + 5% commission on net MRR that naturally aligns the founder with the growth investors expect. If the business doesn't grow post-Y1, the founder only earns the base; if it grows, commission scales. Zero risk of "founder takes enterprise pre-revenue" (burn red flag) and zero risk of "founder takes nothing" (sustainability red flag · sub-optimal decisions from personal pressure).

Priority hires (next 12 months) — 100% cash compensation

1. Head of LATAM Sales (vet) CANDIDATE IDENTIFIED · IN ADVANCED CONVERSATION — the founder is technical, not commercial; without a vet rep there is no real cohort. This hire defines the pace at which we win farms as prospects and convert them into paying customers. Senior candidate with institutional relationships in SAG (Chile's agricultural authority) currently in advanced conversation — onboarding subject to confirmation pre-seed close (profile under NDA).

2. Senior engineer for system review — technical codebase audit + security review + observability + second pair of eyes on architecture. The founder has coded the system solo; before scaling users, a senior peer must validate critical hot-paths. Both hires start within the first month post-seed close. Target profiles + warm candidate pipeline under NDA.

Pre-seed bonus: ACCOUNTANT ALREADY CLOSED In-house accounting professional already identified and committed — integrates Month 1 without a search. This offloads the founder from bookkeeping/IVA/F29/F22 from day 1 and returns focus hours to product/sales.

Entire team based in Chile · remote-distributed · zero offices outside Chile until the market justifies it. Zero equity to employees. Competitive cash compensation + performance bonus + sales commission. No ESOP pool, no dilution from hires. Founder retains full cap-table control aside from external investors.

| Role | Month | OTE USD/month (cash) | Bonus / commission |

|---|---|---|---|

| Head of LATAM Sales (vet, Chile) CANDIDATE IDENTIFIED | 1 | $4-5k | 10-15% commission on closed MRR + quarterly performance bonus |

| Senior engineer (system review + BE/AI) | 1 | $5-7k | 1-2 months bonus at year-end for delivery |

| Engineer #2 (senior FE / mobile) | 4-6 | $3.5-5.5k | 1-2 months bonus at year-end |

| Community Manager (social + online reach + vet/poultry content) | 4-6 | $1.5-2.5k | Quarterly bonus by engagement / leads generated |

| Customer support / onboarding | 6-9 | $1.5-2.5k | Quarterly bonus by NPS / retention |

| In-house accountant ALREADY CLOSED · READY TO INTEGRATE | 1 | $2.5-4k | Professional already identified and committed pre-seed close · joins Month 1 alongside the team |

| Compliance Officer / Legal (post-Series A) | 10-12 | $3.5-6k | Year-end bonus |

Professional services — per-service fees (no equity)

FarmLogU policy: zero equity to advisors, mentors or consultants. If we need specific expertise we hire by project with cash fees. The cap table is reserved for the founder and external investors.

| Service | Modality | Typical fee |

|---|---|---|

| Senior vet consulting (poultry) | Hourly or monthly retainer | $80-150/h · $1,500-3,000/month |

| LATAM compliance advisory | Hourly ad-hoc | $100-200/h |

| Founder mentor / coach (M&A, fundraising) | Per-session | $200-400/h or flat session |

| SAG / regulatory consulting | Fixed project | $1,500-5,000 / project |

Financial projections — high-level summary

Macro target milestones · base case

| Stage | Paying customers | MRR (USD) | ARR (USD) | Verticals · countries · headcount | Milestone |

|---|---|---|---|---|---|

| Today (pre-seed) | 0 paying · 1 pilot | $0 | $0 | 1 vertical (poultry) · 1 country (Chile) · 1 founder | Product live · Seed round open |

| Y1 · Month 12 | ~300-400 | ~$30-36k | ~$360-432k | 1 vertical · 1-2 countries · 4-5 people | Expansion cohort validated · NRR >105% |

| Y2 · Month 24 (Series A trigger) | ~700-1,000 | ~$60-90k | ~$720k-1M | 2 verticals · 3 countries · 8-10 people | Series A raised · 2nd vertical in validation |

| Y3 · Month 36 (path to break-even) | ~1,500-2,500 | ~$150-275k | ~$1.8-3M | 3 verticals · 5 countries · 15-20 people | EBITDA approaching positive · B2G regulator 1-2 countries active |

⚠ Ranges above are base-case ball-park built on standard LATAM B2B vertical SaaS cohort assumptions (see Appendix B · benchmark KPIs). NOT FarmLogU's own data (pre-revenue). Cohort retention curves, monthly CAC payback period, disaggregated monthly burn model, pessimistic/base/optimistic scenarios with sensitivity per key variable (churn, ARPU, CAC, expansion rate) available in the data room post-mutual NDA.

Operating costs — high-level summary

High-level operational policy

- Single HQ in Chile with physical office from day one — target location: Metro Manquehue area, Las Condes (Santiago). Reason: the on-premise AI workstation needs space + stable electrical conditions + focused founder work without distractions. Remote-distributed team joins from Month 3.

- On-premise AI compute from day one (own workstation, no cloud rental). 24-month TCO several times lower than equivalent reserved cloud GPU.

- Minimalist cloud stack: edge infrastructure + dockerized backend + managed DB. Target margin in industry-standard B2B SaaS range.

- Vet-led go-to-market: sales force with veterinary credentials (not generic SDRs). Conversion validated in analogous industries (Veeva, Procore, Toast).

- External services instead of in-house while team < 10 people: accountant, legal, auditor, comms.

- Physical expansion to other LATAM countries: only when local MRR justifies it. Until then 100% online reach from Chile HQ.

Infrastructure cost structure — high level

- Zero hardware CapEx: cloud-only architecture (dockerized backend + managed DB + global edge) with elastic horizontal scale. Exception: on-premise AI compute (own workstation) — 24-month TCO several times lower than equivalent rented cloud GPU.

- Marginal cost per active customer (scale 100-500 accounts): ball-park USD $4-7/month. Multi-tenancy Postgres with RLS + shared cache amortizes the fixed cost across all accounts.

- Projected marginal cost at 1,000+ account scale: USD $2-4/month via economies of scale (DB, observability, AI inference amortized over a larger base).

- Projected gross margin: >80% from Month 6 cohort onward (industry-standard vertical multi-tenant B2B SaaS). Supports the accessible pricing model without compromising unit economics.

- Stack categorical buckets: Cloud compute · Managed database · Transactional email · Payment processor (MercadoPago LATAM) · AI inference · Observability + logging · CDN/edge. No specific vendor names in the public deck.

Bill-by-bill detail · vendor names · cohort cost evolution · 24-month projection · per-scenario sensitivity analysis available under mutual NDA.

Ball-park monthly OpEx per stage (approximate numbers)

| Stage | Team | Total OpEx/month USD (approx) |

|---|---|---|

| Today (pre-seed) | Solo founder | ~$5-7k |

| Month 3-4 post-seed | + 1 vet sales + minimal infra | ~$10-15k |

| Month 6-9 | + 1-2 engineers + CS | ~$20-25k |

| Month 12 (4-5 people) | Consolidated team pre-Series A | ~$30-40k |

| Month 18 (Series A trigger) | ~8 people | ~$50-70k |

| Month 24 (post-Series A) | ~12 people | ~$80-100k |

These are ball-park approximate numbers. Real pricing may vary at the time of hiring each service or person (FX, labor market, vendor pricing, events). Bucket breakdown, runway per stage, salary policy by level, vendor lock-in evaluations and AI hardware roadmap: data room post-NDA.

Round + use of funds

SEED $500k USD · pre-money valuation $4-6M · target dilution 10-15%

Tentative structure

SAFE + Seed tranches to be defined with the lead investor. Public pre-money valuation range $4-6M USD, subject to the final negotiated structure.

Use of funds — distribution and milestones

| Bucket | % | USD approx | Milestones covered |

|---|---|---|---|

| Engineering + product | 60% | ~$300k | 2 hires (vet rep + senior engineer) · stack scaling · LogU AI inference · feature roadmap Q1-Q4 |

| Go-to-market (GTM) | 25% | ~$125k | Vet rep commissions · vet/poultry content · onboarding tooling · industry events · Companion network |

| Legal + compliance | 10% | ~$50k | Term sheet · B2G regulator contracts · INAPI additional classes · k-anonymity privacy · local + international counsel |

| On-premise AI hardware | 5% | ~$25k | Training + inference workstation (24m TCO several times lower than equivalent reserved cloud GPU) |

| Total | 100% | ~$500k | 24-month target runway · Series A trigger at Month 12-15 if MRR > $30k confirmed |

Disaggregated USD amounts per month, expected runway per scenario (pessimistic/base/optimistic), detailed SAFE/Seed structure and granular cohort financial model available in data room post-mutual NDA + confirmed minimum ticket commitment.

Next round — Series A (high level)

Triggered upon reaching MRR / ARR threshold (LATAM SaaS benchmark model). Valuation and terms to be defined with the target lead fund profile. Profile + list of target funds under NDA.

Projected cash flow — 24 months post-seed (approx USD, rounded)

Ball-park internal estimates. Assumes seed close at Month 0 + vet-led ramp-up + staged hires. Detailed model with sensitivity (pessimistic/base/optimistic) in data room post-NDA.

| Period | Cash in | MRR/month (end) | OpEx/month | Cash balance (end) | Key milestone |

|---|---|---|---|---|---|

| Q0 — Month 0 | +$500k seed | $0 | ~$6k | $500k | Manquehue office + AI workstation |

| Q1 — Months 1-3 | — | ~$1k | ~$23k | ~$430k | Vet rep + senior engineer + accountant (already closed) · first 25 customers |

| Q2 — Months 4-6 | — | ~$5k | ~$28k | ~$355k | Hire eng #2 (FE/mobile) · 75 customers |

| Q3 — Months 7-9 | — | ~$12k | ~$38k | ~$265k | Hire CS / Community · 175 customers |

| Q4 — Months 10-12 | — | ~$22k | ~$45k | ~$235k | 300 customers · Series A trigger |

| Q5 — Months 13-15 | +$2M Series A | ~$32k | ~$70k | ~$2.18M | 2nd vertical scoping · 500 customers |

| Q6 — Months 16-18 | — | ~$50k | ~$95k | ~$1.92M | 700 customers · launch vertical 2 |

| Q7 — Months 19-21 | — | ~$70k | ~$120k | ~$1.55M | 950 customers · 3 active countries |

| Q8 — Months 22-24 | — | ~$95k | ~$140k | ~$1.10M | 1,200 customers · break-even near |

Seed $500k distribution per bucket (24 months)

- Engineering + infrastructure ($300k · 60%): two engineers + on-premise AI workstation + cloud + tooling + dev buffer.

- Go-to-market ($125k · 25%): vet rep OTE 12 months + industry events + content + MRR commissions.

- Legal + compliance ($50k · 10%): CL + LATAM counsel + audit + INAPI + corporate structure.

- Hardware + equipment ($25k · 5%): AI Tier 1 workstation + hires' laptops + peripherals + UPS.

Reading: the seed covers runway through Month 12 with buffer; Series A trigger is anchored to validated MRR (not cash burn). The plan does NOT depend on an immediate Series A — if Y1 MRR is below benchmark, the founder meets plan by adjusting hire timing rather than raising a bridge.

Strategic narrative

- Industry electrification doctrine: the LATAM agricultural industry has been stagnant in its digitalization for decades. Our thesis is to introduce modern SaaS infrastructure that catalyzes the transition. If other players follow the same path, better for the ecosystem; if not, we still move forward. Success metric = # of new digitalized producers + reduction of LATAM chicken imports, NOT market share against competition.

- Open market / No monopoly: public APIs, open traceability spec, zero regulatory capture, NO commissions to officials. We accept losing $2-5M ARR Y3-Y5 vs a monopoly play.

- Zero corruption: zero bribes, 12-month cool-off post-resignation, semi-annual interest declarations, whistleblower channel, annual external audit post-MRR.

- Modesty / Facts-first: "Be the best without saying we are the best." Zero superlatives in copy, only facts + metrics + third-party testimonials.

- Neutral Spanish as educational vector: we elevate LATAM rural negotiations through correct grammar. ~16M exposures/year = passive mass education.

Supplementary material + how to proceed

A · Cap table policy — high level

The founder remains the majority shareholder (>50%) in ALL projected rounds — through exit. No Series C planned that dilutes below majority. Few select investors per round, each with a significant ticket. NO crowdfunding. NO shotgun of 20 small angels. Zero ESOP. Zero equity to advisors.

- Seed: maximum 30% delivered to investors → founder retains 70% post-Seed.

- Single lead investor (wanting the full 30%): must write a check for the TOTAL round amount. Ownership disproportionate to capital deployed is not accepted.

- Syndicate (multiple co-investors): the 30% is split proportional to each ticket. 1-2 leads + 2-4 angels co-investing is an accepted structure.

- Later rounds (A/B): dilutions evaluated per individual round, always defending majority >50%. If the math breaks majority, ticket / valuation is adjusted or the round is declined.

Any future round requiring dilution below 50% requires explicit case-by-case founder approval; it is not the default. Alternatives to traditional equity (venture debt, revenue-based financing, dual-class structure) are evaluated before going below majority.

Implication for investors: FarmLogU is looking for investor(s) that respect this policy. Term sheets with full-ratchet anti-dilution clauses or aggressive mandatory pro-rata do not fit the model. It is a deliberate founder selection bias, aligned with long-term vision and continuous strategic control.

Projected cap table per stage with exact percentages per round + target KPIs (CAC, LTV, NRR, gross margin, Magic Number, payback period) available in the data room post-NDA + minimum ticket commitment.

B · Target KPIs (industry benchmarks)

Financial model projected over industry-standard LATAM B2B vertical SaaS benchmarks. Ball-park table below with FarmLogU internal targets vs industry ranges — pre-commercial validation.

| KPI | Industry range (LATAM vertical SaaS) | FarmLogU Y1-Y2 target |

|---|---|---|

| NRR · Net Revenue Retention | 105-115% (top quartile) | 105% Y1 → 110-115% Y2+ |

| Gross margin | 75-85% (vertical SaaS) | >80% from Month 6 onward |

| CAC · Customer Acquisition Cost | $200-600 USD (LATAM B2B vertical) | $300-500 (vet-led GTM) |

| LTV · Customer Lifetime Value (3yr horizon) | $1,500-3,000 USD | $2,000-3,000 base case |

| CAC payback | 12-18 months (healthy) | 9-15 months (vet referral) |

| LTV/CAC · efficiency ratio | 3-5× (healthy target) | 3.5-5× target |

| Magic Number | 0.5-1.0 Y1 / 1.0+ Y2+ | 0.7-1.0 Y1 → 1.2+ Y2 |

| Burn multiple | 1.5-3× (capital-efficient) | 2-3× through Month 12 |

| Blended ARPU | $50-150/mo USD (LATAM vertical) | $80-100/mo blended |

| Annual customer churn | 8-15% B2B vertical | 10-12% Y1-Y2 target |

| Sales cycle | 30-90 days (Starter) · 90-180 (Enterprise) | 30-60 (Starter) · 90+ (Enterprise) |

| Runway per stage | Seed: 18-24 months | 24 months (detailed Q0-Q8 cash flow) |

⚠ All ranges above are industry benchmarks for LATAM B2B vertical SaaS, NOT FarmLogU's own data (we are pre-revenue · 1 operational pilot · no MRR yet). Real commercial validation begins with the seed investment + go-to-market. Sensitivity analysis with pessimistic/base/optimistic scenarios + granular cohort model + per-KPI assumptions available under mutual NDA.

C · How to proceed (process for interested investor)

- Initial email to jadelsolara@egglogu.com with: fund / vehicle name, target ticket (minimum $50k USD), investment thesis, expected timeline.

- 30-minute call (free) — technical alignment, model alignment and preliminary terms.

- If there's a fit: standard mutual NDA (free, no monetary fee).

- Full data room access: projected IRR / MOIC, granular unit economics, detailed cap table, financial model with sensitivity analysis, technical stack, product roadmap, pipeline conversations, term sheet draft. Assisted DD sessions with the founder as needed.

- Term sheet: within FarmLogU parameters (founder >50% permanent, zero ESOP, zero advisor equity, no aggressive anti-dilution clauses).

Operational honesty: we are pre-revenue (1 active operational pilot · MRR still at zero). The process above does NOT include a DD commitment fee today. Once validated commercial traction exists (post-MRR confirmed), the policy may evolve to "data room fee creditable to the investment ticket" as an additional filtering mechanism.

D · Glossary of terms

Quick definitions for the technical terms used in this deck, so the reader doesn't need a specific background in VC, agriculture, tech or LATAM regulation.

Market & finance

- TAM (Total Addressable Market): total market available if your product were 100% adopted.

- SAM (Serviceable Addressable Market): portion of TAM your solution can realistically serve.

- SOM (Serviceable Obtainable Market): portion of SAM you can capture in N years.

- MRR / ARR: Monthly / Annual Recurring Revenue.

- ARPU: Average Revenue Per User per month.

- CAC: Customer Acquisition Cost.

- LTV: Lifetime Value. Net revenue a customer generates over their lifetime.

- NRR: Net Revenue Retention. % of cohort revenue retained year over year (upgrades minus churn).

- MOIC: Multiple On Invested Capital. How many times the investment multiplied at exit.

- IRR: Internal Rate of Return, annualized.

- Payback: months to recover CAC.

- Burn multiple: cash burned divided by net new ARR.

- Runway: months of operation covered by available cash.

Investment structure

- SAFE: Simple Agreement for Future Equity. Instrument that converts to shares in the next round.

- Term sheet: non-binding document with preliminary investment terms.

- Pre-money / post-money: valuation before / after the investment.

- Dilution: % of ownership the founder loses when new shares are issued.

- Pro-rata: investor right to participate in future rounds to avoid dilution.

- Anti-dilution / full-ratchet: clause that protects the investor if the next round is at a lower valuation (full-ratchet = aggressive, adjusts to the lowest price).

- ESOP: Employee Stock Option Pool. Shares reserved for employees.

- Cap table: capitalization table with % per shareholder.

- NDA: Non-Disclosure Agreement (mutual confidentiality).

Technology

- SaaS: Software as a Service. Subscription cloud software.

- ERP: Enterprise Resource Planning. Integrated business management software.

- PWA: Progressive Web App. Web app that behaves like native, including offline.

- IoT: Internet of Things. Connected devices (sensors, equipment).

- MQTT: open standard messaging protocol for IoT.

- AI: Artificial Intelligence.

- Multi-tenant: architecture where multiple organizations share infrastructure with data isolation.

- Edge: globally distributed server network for minimal latency.

- RLS: Row-Level Security. Database-level data isolation per row.

Poultry & agri industry

- FCR: Feed Conversion Ratio. Kg of feed needed to produce 1 kg of egg or meat.

- ADG: Average Daily Gain (body weight/day). Cattle standard.

- Flock / batch: group of birds of the same age and management.

- Broilers: meat-type chickens.

- GS1: international product identification and traceability standard.

- HPAI: Highly Pathogenic Avian Influenza.

- Biomass: live kg per m² or m³, aquaculture metric.

Regulators & legal

- SAG: Agriculture and Livestock Service (Chile).

- SENASA: National Animal Health Service (Argentina and Peru).

- SENASICA: National Service for Agri-Food Health, Safety and Quality (Mexico).

- MAPA: Ministry of Agriculture, Livestock and Supply (Brazil).

- USDA APHIS: Animal and Plant Health Inspection Service (USA).

- FAO: Food and Agriculture Organization (UN).

- SpA: Sociedad por Acciones (Chilean legal structure).

- INAPI: National Industrial Property Institute (Chile, trademark registry).

- SII: Internal Revenue Service (Chile).

- CMF: Financial Market Commission (Chile).